Micron Technology ($MU) - Part 2

Micron Technology ($MU) - Part 2

Introduction

In the previous analysis of Micron, I proposed recommendations to Micron’s management from the perspective of an investor to increase Micron’s long-term value. This post will focus on the more in depth analysis of my recommendations. Unfortunately, Micron’s Investor Relations team has not gotten back to me yet. As such I’ll be unable to provide responses to my questions for the foreseeable future. I’ll share if and when I hear back.

Update on Thesis

After some thought, I need to update my original recommendation as I realize that I did not properly clarify my approach to potentially investing in Micron. I have not yet invested in Micron due to some concerns over the state of the global economy and financial markets. While I believe that they can generate value long-term, their current price (relative to my IV of ~$82) does not provide an adequate margin of safety for me to invest.

The adjusted recommendation is a BUY rating on Micron should the price drop to ~$50-55. Given Monday’s market declines, I personally think there’s more room for things to get far worse before they get better across the board. In normal times, $50-55 is reasonable, but I will be waiting for ~$40-45 if not lower.

TL; DR

Eliminate Storage Business Unit. Financially, I don’t personally think the Storage Business Unit (“SBU”) is adding much to Micron’s valuation (based on what I understand wihtout speaking to someone at the company). Even in scenarios where Micron does not have to invest as much in the remaining divisions, their valuation is close enough to the current stock price that I would consider the SBU zero value-add

Increase Buybacks and Dividends. Micron can maintain its current buyback rate (as a percent of free cash flow) and increase its dividend 10x to $4.00 / share (~7% dividend yield per annum) and still maintain a cash position of ~$4-5bn at the end of each quarter

Please feel free to email me directly or leave a comment with any questions.

Disclosure: I do not own any shares in Micron Technology Inc. Any investment in Micron will be disclosed at a later date. This post is intended for educational purposes only, and anyone seeking to invest in Micron should conduct their own analysis and due diligence prior to investing.

Recommendations to Management

Review strategic value of the SBU business unit – assuming that the reason for the lower operating margins in this segment are due to lower priced products (storage products are cheaper than ever before), there is potential value in redirecting the R&D initiatives from this division towards end-markets with more positive long-term outlooks (i.e., automotive, computing, AI, quantum computing, etc.)

Develop a plan to return cash to shareholders over the next three to five years via increased dividends (~$4.00 / share annually) and stock buybacks

Recommendation 1 - Eliminate Storage Business Unit

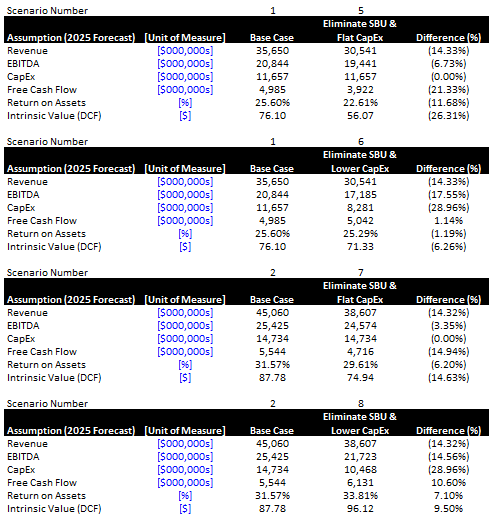

The updated model has a few new scenarios (Scenario 5 - 8) that analyze Micron’s future performance based on the assumption that the Storage Business Unit (“SBU”) is eliminated.

Some key assumptions were made in developing these scenarios:

Revised Operating Profit = Original Operating Profit - SBU Operating Profit

For simplicity, I’ve just created a second “Actuals” tab (“Adj. Actuals”) that has revenue and estimated operating expenses for the SBU removed from the income statement

SBU Operating Expenses are eliminated based on the % of revenue the SBU generated on a quarterly basis

All other financials are assumed to remain consistent. For example, while there would be a difference in inventory, accounts receivable, etc. based on this change, but a lack of supporting assumptions to estimate the variance

The key assumption on Micron’s future valuation is tied to how its CapEx budget is reallocated. For example, if Micron is able to reduce CapEx due to lower facility utilization via the elimination of this division, its valuation will be higher. Conversely, if CapEx remains flat relative to the original forecast (Scenarios 1 and 2), Micron’s valuation would be lower unless the remaining three divisions increase sales

Findings

Assuming that the only material changes to Micron’s forecast come through the income statement, Micron’s value does not materially change by eliminating its SBU division.

In my base case scenario (Scenario 1), Micron’s IV is ~$76 (~7% revenue growth per annum), and in the equivalent scenario (Scenario 6) where Micron reduces CapEx, the IV falls to just ~$71.

Using Micron’s long-term revenue growth forecast of ~14% (Scenario 2), Micron’s IV is ~$88, and in the equivalent scenarios with flat CapEx, the IV is ~$75, which is above Micron’s closing price of ~$58 (as of 2022/06/13).

I’ve presented a comparison of the 2025 forecasts for the various scenarios below, to provide insight into the longer term impacts.

Note that in the right hand column for Scenarios 5 - 8, the only price below the current market price is Scenario 5, which due to broader market declines is now close to the minimumIV. This is due to a relatively low growth rate (~7% annually) and the CapEx allocation as a share of revenue increasing.

Strategic Value

A potential argument to counter shutting down the SBU would be “Why would a company that’s in the business of making memory chips not sell its products to storage-solutions providers?”

My response is simple - just because they make memory chips doesn’t mean their a storage-solutions provider. Micron’s core competency is in manufacturing memory chips, not enabling data storage providers. The pricing of memory storage solutions has been decreasing (see the picture below from Part 1 charting memory and storage costs from John C. McCallum).

If this broader pricing trend continues across the remainder of its segments, Micron’s margins will compress over time and it will need to identify alternative paths to maintain / increase margins and cash flows.

Recommendation 2 - Increase Return of Capital to Investors

I also recommended that Micron significantly increase its returns of capital to shareholders. Micron’s current dividend is $0.40 / share, representing a dividend yield of ~0.6% per annum.

Micron has also repurchased ~$667m in equity over the past two quarters, representing ~40% of their quarterly free cash flow. While this is significant, I am not sure if this trend will continue (and my base case assumes ~20% of free cash flow is allocated to share buybacks).

Findings

Micron can maintain a cash position of ~$4-5bn over the next five years, while maintaining a long-term share buyback rate (as a percent of free cash flow) of ~35-40%, and increase its annual dividend 10x to $4.00 / share, representing a dividend yield of ~7%.

Given the risk that pricing in the long-term may decline, I would argue that it is imperative that Micron begin immediately returning cash to shareholders to ensure that any excess cash held on its balance sheet is not wasted.

The current economic volatility, specifically related to inflation, means that this cash is worth less and less to Micron. Micron’s capital projects require years, not months, to complete, so it is unlikely that they will pursue any major capital investments to grow their business while economic volatility remains high. This cash would be better utilized in shareholders pockets where it can be reinvested.

Notes

Thanks for reading - if you enjoyed reading this, and would like to support, please subscribe and share using the links below. Thank you to everyone who responded to the survey. This has helped me put together a schedule of topics for the next three months or so.

The next edition of The Simple Investor will be an overview of the Canadian cannabis industry and how I saw things developing, as well as some company-specific notes and analysis of how excise duties are calculated.

Please feel free to email me directly or leave a comment with any questions.

Cheers,

Kian