Micron Technology ($MU) - Part 1

Introduction

This report will focus on Micron Technology Inc. and its strategic positioning in the global semiconductor industry.

Micron is a semiconductor company that designs, develops and manufactures memory and storage products for a variety of industries, with the vision of “transforming how the world uses information to enrich life for all”.

TL; DR

Investment Thesis. BUY (Intrinsic Value of $76-88) – Micron has the potential to initiate a capital return program to shareholders via buybacks and/or dividends due to their growing cash position (estimated to reach at least $13bn by the end of 2023)

Industry Growth. Semiconductors are becoming increasingly important in multiple products and services being offered worldwide, and the industry is potentially going through a secular shift to a demand-driven model that will increase the predictability and stability of cash flows for all market participants

Operational Efficiency. Micron’s operational performance, while cyclical, has been improving over the long-term. With proper capital management, Micron can continue its strong operational performance supported by consistent end-customer market growth

Please feel free to comment on this post with any feedback or questions.

Disclosure: I do not own any shares in Micron Technology Inc. Any investment in Micron will be disclosed at a later date. This post is intended for educational purposes only, and anyone seeking to invest in Micron should conduct their own analysis and due diligence prior to investing.

Industry Overview

Semiconductors are essential pieces of technology that are a component of electronic devices, enabling advances across multiple industries and technological applications.

The semiconductor industry is highly competitive that involves capital-intensive operations that include near-vertically integrated operations to ensure customers are receiving leading-edge technology in an ever-changing environment. A leading semiconductor company must have strong capabilities in research, supply chain, talent, IP management and protection, and regulatory compliance. As more “things” require technological innovations, from cars to refrigerators, the underlying demand for semiconductors will continue to scale, all while consumers demand more advanced products.

As global economic and geopolitical instability becomes a pervasive theme, semiconductor companies must ensure they remain agile while continuing to advance the rapid development of sophisticated and integral technologies that support the broader technology community.

One of the earliest predictions of the increased complexity in the development of integrated circuits was that the number of transistors on an individual chip would double approximately every two years. This prediction, made in the mid-1960s by Gordon Moore has held true over the past half century, and the semiconductor industry is now only seeing a slowdown in the growth of the number of transistors on individual chips.

In line with Moore’s law, the number of transistors on a chip roughly continued to double every two years between 2010-2020, and the complexity of individual chips has increased dramatically all while the individual chips are becoming smaller.

Source: Visual Capitalist – Moore’s Law

As these requirements become more pronounced, the overall semiconductor industry is being dominated by fewer and fewer players, where, while economic profits are growing significantly, a smaller group of major players is beginning to dominate the market. The slightest improvement or advantage to a single player’s products has generally resulted in said player earning an outsized market share due to these “winner take all dynamics”.

As such, it is imperative that any company wishing to be a serious competitor in the global semiconductor industry must be well capitalized to maintain a strong operating base and R&D capabilities.

Source: McKinsey

Please see Appendix B for more information on the semiconductor industry.

Strategic Positioning

Micron Technology is a US-based semiconductor company, and is the fourth largest semiconductor company in the world (by revenue, excluding IP/software revenue), with operations in 17 countries, including 11 manufacturing sites, and 18 customer labs. Micron also recently surpassed more than 50,000 patents for its current and future technology.

Each of Micron’s four business units serves a variety of markets for different technological needs, with a specific focus on providing semiconductors that leverage DRAM and NAND technologies:

DRAM. Dynamic random-access memory is typically used for the data or program code required by a computer processor to function (source)

NAND. Non-volatile, re-writable storage that does not require power to retain data (source)

Micron serves four primary markets, which are:

This limited focus on a core group of memory chips that are usable across multiple end markets can continue to shelter Micron from the potential boom-bust cycles that have existed in the semiconductor industry.

Another key factor in favour of Micron’s long-term growth is that 70% of growth in the semiconductor industry by 2030 is predicted to be driven by three industries: automotive, computation and data storage, and wireless.

Segment Analysis

Micron provides sufficient data to summarize the segment specific performance (specifically revenue growth and operating margin), as seen in the table below:

Micron’s largest segments fortunately generate the majority of its operating profit, although the relative underperformance of the Storage Business Unit is a potential drag on long-term value generation.

Note: I will be reaching out to Micron Investor Relations and management to inquire further about why this segment underperforms, and the strategic value of maintaining this division.

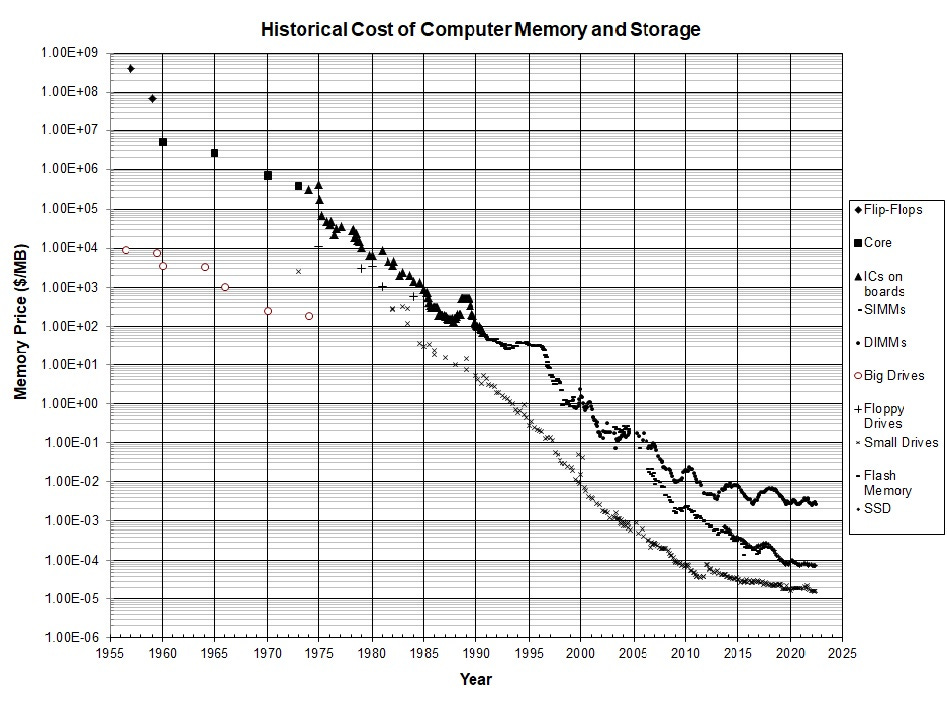

Source: John C. McCallum via Fabricated Knowledge

Assuming that Research & Development, and Selling, General & Administrative Expenses are allocated proportionally to the SBU segment (as a percentage of revenue), Micron could increase its margins (gross margin and operating margin) by eliminating this segment.

Note: A more comprehensive analysis of the impact to Micron’s cash flow and intrinsic value is underway and will be the subject of a later post. This post will also include as many responses as possible to my questions for management.

Edit: Operating Profit (excl. Restructuring & Other) in the “Close SBU Segment” was calculated by removing SBU Operating Profit from the actual Operating Profit (excl. Restructuring & Other). R&D and SG&A expenses we’re prorated based on SBU Revenue as a % of Total Revenue. Due to differences in SBU Operating Margin and SBU Revenue as a % of Total Revenue, the difference will be allocated Other Operating Expenses.

Competitive Analysis

Source: roic.ai

Individual company valuations significantly delineate based on a group’s operating margin and RoIC, and Micron is one of the larger and more efficient companies in the industry.

NVIDIA and AMD have received relatively premium valuations to the other three US-based semiconductor companies in part driven by the uptake in retail investors at the start of the COVID-19 pandemic.

Note: I do believe that NVIDIA deserves a relative premium valuation due to its brand equity within the gaming industry and its operational efficiency (high operating margin and RoIC).

Valuation

This valuation was approached in two stages:

Initial / Pre-Model Thesis. Prior to building the financial model, I reviewed Micron’s 10K from 2021 and other articles about the semiconductor industry to: 1) understand the key drivers; 2) understand Micron’s high-level strategic positioning; and 3) outline an initial thesis and guesstimate of variance to intrinsic value (“IV”) (not an exact dollar estimate, but rather the expected relative outcome to the current price based on a discounted cash flow (“DCF") analysis )

Concluding / Post-Model. Once a quantitative analysis of the business was complete, certain core theories were validated, and questions for management were prepared

Valuation Methodology and Conclusions

Since I began analyzing individual companies, I have generally completed two separate analyses: 1) a DCF; and 2) multiples.

For Micron’s valuation, the DCF is more accurate due to Micron’s relative undervaluation to the semiconductor industry.

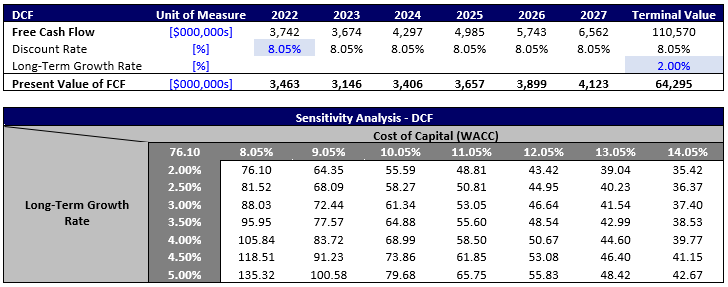

DCF Analysis

Based on a DCF analysis of Micron’s future cash flow, I estimate that Micron’s intrinsic value is between $76-88. The baseline of $76 assumes revenue growth of approximately 7% from 2022 to 2027, while the upside case of $88 is based on Micron’s internal guidance of approximately 14%.

Multiples

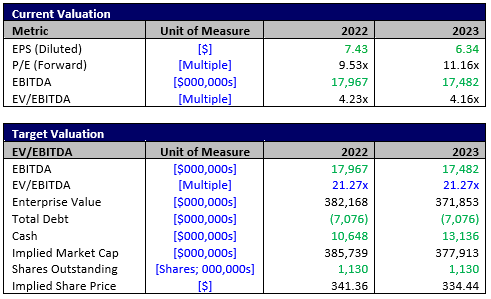

Based on an analysis of Micron’s current valuation relative to the overall semiconductor industry, Micron is severely undervalued (by approximately 80%). As noted, I am not basing my valuation on these multiples, but it is helpful context in the low-probability scenario (< 10% confidence) that Micron’s valuation increases solely due to multiple expansion to better align with the industry.

As noted, I do not believe that the above valuation accurately reflects Micron’s IV, but am sharing to provide context to the relatively high valuations of the entire semiconductor industry.

It is also important to note that the “upside” case based on 2023 EBITDA is actually lower than the “base” case on 2022 EBITDA. This is due to a decline in EBITDA and earnings in 2023, driven by lower gross margins (driving EBITDA down), as well as higher borrowing costs (driving earnings down).

Initial / Pre-Model Thesis - HOLD

Date: 2022/05/09

Overall, Micron appears to be a leading semiconductor company. While all major semiconductor manufacturers are B2B, Micron appears to be positioned as an enabler of IoT across consumer staples (autos, computers, other home appliances although not explicitly stated)

Overall competitive advantages (based on customer reviews on Amazon) appear to be very favourable, and likely represent a statistically significant enough sample size of customers to be reliable

Multiple products on Amazon with >20,000 reviews and 4.5 stars or more (three products with >55,000 reviews are 5 stars)

Assuming notes related to “leading position” and “first launches” of certain innovative products are indicative of the overall leading position, Micron likely has the tools to be successful in the long-term

Power to become a top player, assuming aggressive long-term consolidation will be dependent on completing a financial model incorporating long-term industry growth and market share trends

Encouraging note is that Micron’s end customer base appears to be diverse enough to withstand any cyclicality in the semiconductor industry

Valuation Prediction - shares will be trading near IV (based on a DCF)

Concluding / Post-Model Thesis - BUY

Date: 2022/05/17

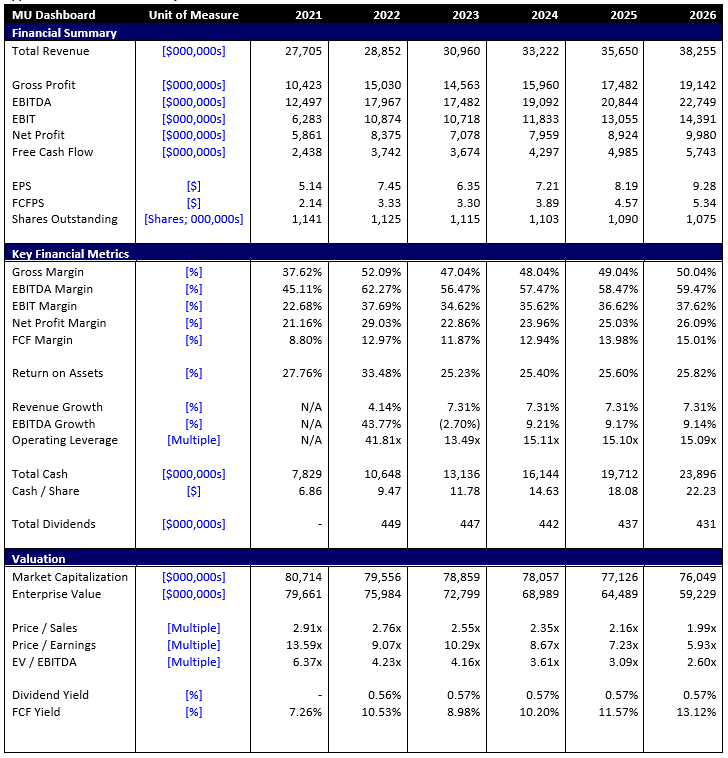

Micron generates significant cash flow from its operations that will provide it with a war chest of over $10-15bn by 2023

Micron does not require any of this incremental cash to fund operations, and while there is no minimum cash level required, the continued growth in excess cash would warrant some sort of return to shareholders

Micron is severely undervalued when analyzing its multiples relative to the semiconductor sector:

~4.4x Micron EV / EBITDA vs. ~21.3x Industry

~9.9x Micron P/E vs. ~66.3x Industry

Micron’s fair value is ~$82, though with growing excess cash, management should tactically return capital to shareholders thus creating a higher probability of upside due to operational stability

Micron’s diversity of revenue-generating industries mean that it will be able to withstand any sector shocks that other companies such as Intel, AMD or NVDA may be exposed to

Valuation Conclusion - shares are approximately trading at IV based on a DCF analysis

Summary

Micron is currently trading very close to its intrinsic value of ~$82 (average of Scenarios 1 and 2) vs. a current price of ~$69 (as of May 19, 2022).

However, Micron is trading at significantly lower multiples than the semiconductor industry as a whole (~4.4x Micron EV / EBITDA vs. ~21.3x Industry; ~9.9x Micron P/E vs. ~66.3x Industry). As such, any price below ~$82 can be considered a reasonable buy price. Micron’s ability to consistently generate cash flow, despite end-market economic cycles will be a key value driver in the long-term.

Micron’s capital management in the coming years will be critically important to shareholder value generation. Micron is currently sitting on ~$9bn in cash, and generates ~$3bn / quarter in operating cash flow. I have forecasted that Micron will have over ~$13bn in cash by the end of 2023, and unless this cash is used for a major investment that is expected to generate significant long-term value, Micron should initiate major share repurchases and increase its dividend to ~$4.00 / share annually.

Micron should be considered a long-term buy due to its cash flow generation potential, and relative shelter from economic shocks to the individual sectors in which it operates.

Recommendation to Management

Review strategic value of the SBU business unit – assuming that the reason for the lower operating margins in this segment are due to lower priced products (storage products are cheaper than ever before), there is potential value in redirecting the R&D initiatives from this division towards end-markets with more positive long-term outlooks (i.e., automotive, computing, AI, quantum computing, etc.)

Develop a plan to return cash to shareholders over the next three to five years via increased dividends (~$4.00 / share annually) and stock buybacks

Key Risks

Geopolitical Risk. Micron has operations in Taiwan, which could be at risk of an invasion (similar to Russia’s invasion of Ukraine). If a similar geopolitical shift were to occur, Micron may need to shut down its facilities in Taiwan resulting in significant disruption to its global operations and long-term value

Economic Risk. While Micron’s end-customer markets are expected to grow in the long-term, current concerns over inflation and rising interest rates pose risks to the global economy. An significant slow down in one or more of Micron’s key end-customer markets (e.g., automobiles) could have a disproportionate impact on Micron’s cash flow and value in the next three to five years

Questions for Management

Note: The questions outlined below are questions that I will be posing to Micron’s management and Investor Relations team in the coming weeks. A future post will summarize the responses received.

What are the gross margin profiles for each business unit?

Why is the Storage Business Unit’s operating margins significantly lower than the remainder of the business? What is the long-term value proposition of retaining this division?

How long is the company’s sales cycle? Based on inventory turnover, it appears as though you hold inventory for eight months prior to sale?

What shifts in the market has Micron observed related to large technology companies and automotive OEMs bringing chip design in-house? Would Micron be able to contract manufacture based on a specific customers’ design and demand requirements?

What are Micron’s primary focuses in the R&D strategy? (i.e., new processes, new products, etc.)

Given that the rate of doubling originally predicted by Moore’s law has slowed, what sort of innovation and research is Micron conducting to either maintain the rate of doubling (according to Moore’s law) or find innovation beyond Moore’s law (i.e., new materials for manufacturing that are more sustainable, efficient, etc.)?

Are Micron’s current R&D initiatives focusing on technology for next year? Or technology for ten years from now?

How geographically diverse are Micron’s customers?

What risk-mitigation initiatives is Micron undertaking to become more agile and avoid increasing economic and geopolitical volatility?

How is Micron handling talent management and/or retainment of top talent?

How has Micron repositioned facilities to get their operations closer to end-users and/or the next steps in the supply chain to reduce uncertainty?

How might Micron respond to a potential invasion of Taiwan?

How will Micron take advantage of the CHIPS Act?

What percentage of Micron’s revenue is generated from application-specific integrated circuits?

Appendix A - Financial Analysis

Figure 1 - Key Financial Metrics Index (Historical)

Figure 2 - P/E Multiples (Historical)

Note: P/E multiples are capped at 100x for visual purposes only.

Appendix B – More Industry Information

Historically, the semiconductor market’s success has been dictated by the supply-side of the market, as observed by the underlying boom-bust cycles. Throughout these boom-bust cycles, the entire semiconductor industry has continued to steadily grow revenue.

Source: Semiconductor Industry Association

These boom-bust cycles have occurred while the underlying demand for semiconductors has continued to grow due to the nature of “things” becoming more technology-intensive. The Fabricated Knowledge blog argues that the semiconductor industry may be undergoing a secular shift towards a demand-driven model. “Each year, massive supply is added, yet demand continues to simply outweigh it.”

“This is a simple expression of the law of large numbers – if semiconductors have a positive growth relationship it would mean that the bigger the number of different markets that are not correlated, the closer the aggregate results will approach the underlying trend.” – Fabricated Knowledge

Based on this potential secular shift towards demand-driven dynamics, there is significant potential for existing semiconductor companies to next steps in their leadership positions all while sheltering their businesses and shareholders from cyclicality.

Source: ASML Holding N.V. via Fabricated Knowledge

Due to the capital-intensive nature of the semiconductor industry, companies that are already well established will likely be the long-term leaders, and those that are well capitalized today are positioning themselves for growth through research & development (on improved products and processes) and capital expenditures in new facilities.