Palantir Technologies ($PLTR)

Palantir Technologies ($PLTR)

Introduction

Palantir Technologies is a company that builds software to help organizations integrate their data, decisions and operations at scale.

TL; DR

Investment Thesis. My estimate of Palantir’s intrinsic value is ~$12 / share, using a DCF. As Palantir has strong margins and cash generation (excl. non-cash expenses such as stock-based compensation), I am confident that due to their core value proposition, they can be a leader in the tech space over the long-term. I will personally be seeking to buy Palantir around $5-6 / share

Value Proposition. Palantir’s core value proposition is the ability to offer their customers the ability to make better decisions. On the surface, they have simply built relatively complex tools that can help organizations integrate data. However, when you dig a bit deeper, a more interesting value proposition becomes evident - the opportunity to expand the reach of democratic decision making and process around the world

Qualitative Valuation. While a traditional quantitative valuation is based on financial performance and cash flow generation, one can look at Palantir through a different lens. If you like to think more philosophically, ask yourself the following:

How would you value the ability to increase the probability that every decision you make moving forward would work out as you hoped?

How much would this be worth to you?

Please feel free to comment or email me with any feedback or questions.

Disclosure: I do not own any shares of Palantir Technologies Inc. Any investment in Palantir will be disclosed at a later date. This post is intended for educational purposes only, and anyone seeking to invest in Palantir should conduct their own analysis and due diligence prior to investing.

I previously owned shares in Palantir and liquidated my position in April 2022 due to concerns over the state of financial markets (and the broader economy). I maintain a strong interest in investing in Palantir.

What does Palantir do and why?

Palantir was founded in 2003 with the vision of creating software of changing the way decisions are made in organizations by unlocking insights from a variety of datasets to provide a consolidated view of a specific problem.

Palantir’s name comes from the Lord of the Rings trilogy, and the “palantÍri”, the magical orb that allows the possessor to see anything happening in the world at any time. Conceptually, this description fits very well with Palantir’s mission – if you could see everything going on in your organization in a single spot, you should (in theory) be able to make a more informed (and a better) decision.

Palantir was founded because “when we looked at the available technology, we saw products that were too rigid to handle novel problems, and custom systems that took too long to deploy and required too many services to maintain and improve.”

Palantir therefore built a custom solution for organizations that was nearly ready to be implemented right out of the box, and required minimal end-user customization to become available. Gotham and Foundry are the “custom systems”, and Apollo reduces the amount of “required services to maintain and improve”.

Palantir’s CEO, Alex Karp, does not hide the company’s political motivation to spread the principals of democracy further around the world. I do not wish to comment on the implications of this goal when pursued by a large multinational entity, but it is integral to understanding how Palantir has developed over the past 20 years.

One of Palantir’s earliest investors was In-Q-Tel, the venture capital arm of the CIA, and worked with governments developing technology to improve government insights into the troves of data that were available. It is even rumoured that Palantir’s technology was used to help find Osama Bin Laden (and indicative of the trust some institutions have for Palantir).

This insight into Palantir’s political involvement (whether or not you agree with it), is integral to understanding Palantir’s vision and how it views its value proposition to the world.

Note: It is important to understand that Palantir’s business does have political motivations. If you are interested, please refer to this video and note Alex Karp’s references to morality, “Western” society, etc.

The “Product”

Palantir has built the digital infrastructure to help organizations make more (and better) data-driven decisions. They provide overview videos on each of their main products; Gotham, Foundry, and Apollo. They have also made extensive impact studies available to those interested.

Palantir’s bespoke approach was to build a solution that requires relatively little customization regardless of their customer. This is reflected in the wide variety of customer applications, ranging from auto racing to anti-money laundering.

Gotham. Gotham is primarily used by government and intelligence clients. It enables users to identify patterns that are hidden within datasets and supports the development of real-world responses

Foundry. Foundry is Palantir’s commercial offering, allowing organizations to better organize their data by bringing it into a central operating system. Users are able to integrate and analyze data from a central location, improving the ability to make better informed decisions

Apollo. Apollo enables users to retain access to Palantir’s software on a continuous basis by ensuring the rapid, secure delivery of any software and other updates

Palantir has made a bet that in the future, data and the ability to make decisions with a higher probability of success will become a competitive advantage (similar to how strong brand equity is a competitive advantage).

Business Model

In this section, I will share my view on a few common criticisms of Palantir’s business model and why their stock price has yet to reach (technically return and remain on) the moon.

Customer Base

For some time, there was significant criticism of Palantir’s lack of commercial exposure and until the 2021 fiscal year, much of this progress was ignored. Palantir has more than tripled its commercial customer account since Q4-2020, growing from just 49 commercial customers to 147 in Q4-2021 (184 in Q1-2022).

Palantir has maintained 90 government customers over the same period. Overall, Palantir’s total customer count has almost doubled from 149 customers in Q1-2021 to 277 in Q1-2022.

Personally, I think that the level of trust that the government has put into Palantir’s technology is very important in developing Palantir’s competitive advantage. Gaining this level of trust with major governments (including the United States, Canada and United Kingdom), specifically in the areas of defense, national security, and healthcare is an important marker of their potential effectiveness. Government institutions are by no means the best decision makers on earth, but these customers are sticky and highly valuable.

Recent major signings with the U.S. Space Systems Command (worth ~$175m over the next year), Army (worth ~$36m over 14 months), and commercial organizations like Stellantis (unknown value) reinforce Palantir’s position as a preferred partner for major organizations worldwide.

Through Reddit, we have access to a tracking tool that tracks the majority of Palantir’s commercial and government customers / contracts.

Stock-Based Compensation (“SBC”)

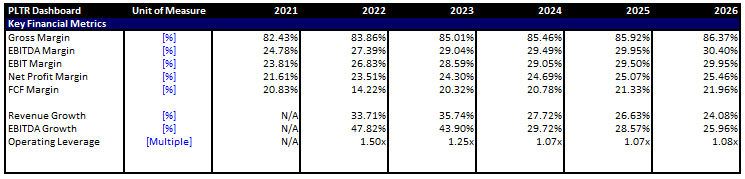

A major criticism of Palantir is its profitability. On paper, it appears as though Palantir doesn’t generate any money (on their income statement), but this is mostly due to significant SBC being given to employees. An analysis without adjusting their financial statements to remove stock-based compensation severely skews the attractiveness of the underlying business.

Palantir has spent an average of $185m on SBC per quarter since the start of 2021, and is primarily responsible for the company’s paper losses. When eliminating SBC from the analysis, Palantir appears to be a profitable and efficient company, as seen below:

Alex Karp has regularly indicated that the reason for Palantir’s massive SBC payments serve two functions:

Attracting and retaining the best people from around the world who are aligned with Palantir’s mission and vision; and

Aligning these employees with the best interests in the company.

On the surface, this lack of profitability appears concerning. When analyzing the income statement further, in tandem with the cash flow statement, it becomes clear that Palantir’s management has implemented a fairly strong business model. If they are able to maintain strong EBITDA and FCF margins over the next five years, I believe that they will be able to justify this level of SBC.

Shareholder Dilution

The long-term impact of SBC payments to employees is the dilution of existing shareholders. These concerns, while valid (analytically) are overblown as the rate of dilution is significantly slower than the rate of growth.

Dilution, while never ideal for an existing shareholder, is not a kiss of death that it is made out to be in day-to-day news cycles. As retail investors, we should not be focused on minor dilution events like rewarding equity to employees. They do the work and deserve part of the upside.

The data below has been indexed to 100 to compare earnings and free cash flow growth, relative to the dilution of shares outstanding.

Valuation

Palantir’s share price performance is highly volatile, and despite increasing by 400% in under six months at the start of 2021, it has since declined so drastically that Palantir (like many other tech companies) is now underperforming the NASDAQ.

I am not knowledgeable enough about technology as a whole to provide a detailed justification as to why tech companies command valuation premiums relative to the rest of the market. However, I do believe that tech companies should command valuation premiums due to technology’s inherent ability to accelerate underlying changes in an organization’s performance.

Palantir is a company whose core offering is designed to help its customers improve their decision-making ability, and drive tangible changes in their performance.

DCF Analysis

Below I’ve summarized my valuation estimates for Palantir.

This scenario is based on ~30% revenue growth through 2025 (in line with Palantir’s guidance). I’ve driven their revenue growth by a combination of growth in new customers and growth in the average value per contract.

Multiples

A 44x EV / EBITDA multiple is too expensive for my personal preference, but leveraging a DCF, Palantir appears to be trading just below its intrinsic value of ~$12.

As with Micron, I am not basing my valuation on multiples – I do not believe that the valuation premium (as noted above) is justified relative to the overall market (~15-20x EV / EBITDA).

Since Palantir has a FCF margin of ~20%, using a DCF presents an ideal valuation methodology.

I will be closely monitoring Palantir’s share price and general market conditions, and once I am comfortable that the current volatility (market and economic) has subsidised, I will seek to make an investment in Palantir.

Summary

Palantir’s core offering is enabling better decision making. This, in theory, has unlimited value to customers, and therefore almost unlimited value to Palantir. This seems like wishful thinking, and it is. But I still think that it’s exciting to find companies that you can analyze through the lens of their benefit to humanity, rather than just on the basis of how they make money.

In learning more about Palantir, I quickly realized that the way the organization presents itself (from the executive team down to their engineers) is very consistent. Palantirians (as they call themselves internally) collectively buy into the notion that their core value proposition and product offering is the ability to make better decisions, not a piece of software.

If someone offered you the ability to increase the probability that every decision you make would generate the desired outcome, what would that be worth to you or your organization?